To get the details on this FIA and the carrier that offers it, click on the following link:

https://advisorshare.com/9-5-percent-guaranteed-cap

Not that any advisor should pick a product based on commissions, but the 5-year product pays a 4.5% commission, and through June, the carrier is offering a 1% bonus (so, 5.5% total commission).

The carrier also has a 10% guaranteed cap on its 7-year product.

FYI, the next best guaranteed cap (S&P 500 index) products

Oceanview: 5-year and 7-year = 8.25%

GILICO: 5-year = 7.75% and the 7-year = 8.00%

Global Atlantic: 5-year = 7.25% and the 7-year = 7.50%

There is a big difference between a 9.5% guaranteed cap and these three other best products.

Eliminating the #1 problem with FIAs

If you’ve sold an FIA in the last 5 years, the chances are high that your client’s renewal cap on the measuring stock index is lower or significantly lower. If you’ve been using Athene, Allianz, and many of the other popular products pitched by most IMOs, that is almost certainly the case.

A great way to get an upset client is to sell them an FIA with an S&P 500 cap of 10% at issue and then two years later have that cap be at 6%.

Stating the obvious…why cap renewal rates matter

The easiest way to understand the importance of renewal caps (besides angry clients when a carrier dumps caps on renewal) is through a comparison.

Let’s look at an example with a carrier that starts with the same 9.5% cap at issue, but then lowers it using the following schedule.

Year 2 cap = 8.75%

Year 3 cap = 8.00%

Year 4 cap = 7.00%

Year 5 cap = 6.00%

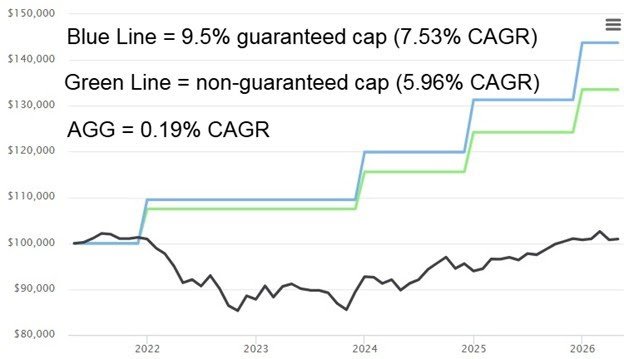

I’ll go back the last 5 years and compare it to an FIA with a guaranteed 9.5% cap.

The following is from our industry-best OnPointe Risk Analyzer software, where I also threw in a comparison to AGG (the U.S. Aggregate Bond Index (the 40% of a 60%/40% stock-to-bond portfolio)).

Which line will your clients like better? The black, green, or blue? I like a 7.53% ROR much better than a 5.96% ROR.

Clients will likes the blue line, and that’s the no-risk line because it’s with the carrier that offers a 9.5% guaranteed cap on the S&P 500 (minus dividends) for five years.

What’s the rub with this carrier? The rub with this carrier is that it’s a B++ carrier. Historically, I’ve stuck to A- or better carriers. Why then am I doing a newsletter on a B++ carrier? Two reasons:

1) We’ve reviewed the financials, and we think they are good.

2) There is little risk when using a 5-year product.

It’s pretty easy to tell when a carrier isn’t the most financially stable, and a B++ carrier that looks like it’s trending to A-, in my opinion, is not a risk when using a 5-year product.

In any event, while my newsletters are usually longer and many times cover more technical concepts/topics, this newsletter is pretty simple.

If you are selling FIAs, you should know about this product.

If you are not selling FIAs because you are worried about the carrier dumping caps, then this product may give you reason to dip your toe in the water.

OnPointe Risk Analyzer Adds the Industry-First AI Portfolio Review Tool

If you missed last week’s newsletter, you missed out on the launch of a new tool that is going to reset the landscape when it comes to “risk tolerance” programs like Riskalyze/Nitro, Hidden Levers, etc. It’s the most innovative tool to hit the risk space in 10+ years.

Advisors will use this tool to help leads understand (outside of the normal risk program metrics) why their current portfolio isn’t very good and why they need to move their AUM to a new advisor.

Download a “Real” Ken Fisher AI-Powered Portfolio Review

AND

Watch an On-Demand Video Overview

To download a 12-page review of a Ken Fisher portfolio AND to get access to watch the webinar on-demand showing how the portfolio review tool works in OnPointe, click on the following link: