Roth IRA conversions are white hot right now as a tool advisors can use to find new clients (ones with large IRA balances). It’s for this reason that we spent time creating the following:

1) Creating the “only” accurate Roth conversion software (OnPointe):

www.onpointesoftware.com/roth-app-sign-up

2) Launched the industry’s ONLY Certified Roth Conversion Specialist™ (CRCS™) designation:

www.certifiedrothconversionspecialist.com

3) Soon, we will be launching our Roth Sherpa™ marketing platform:

www.advisorshare.com/roth-sherpa

4) Our new book: Deconstructing Roth IRA Conversions: Myth vs. Reality

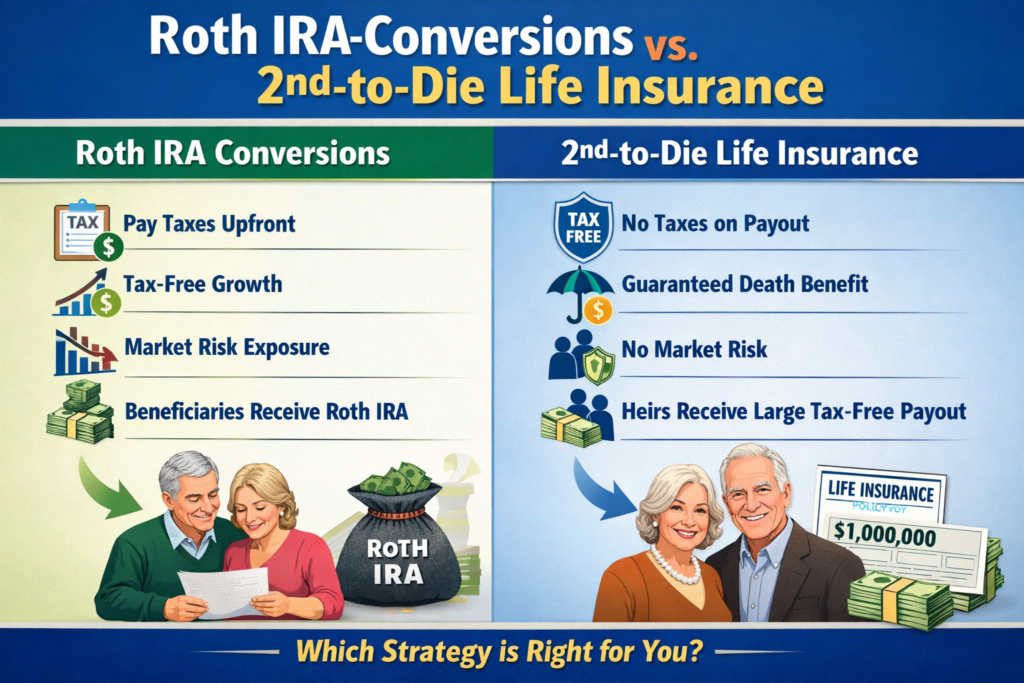

Roth IRA Conversions vs. 2nd-to-Die Life Insurance

Since we rolled out the CRCS™, we are regularly asked if it’s better to buy life insurance on the parents or implement a Roth RIA conversion IF the goal is MORE money for the heirs.

And the answer is….maybe (it will depend on the age and health of the parents)

Liquidate and Leverage (L&L)

The concept of taking systematic distributions from an IRA to uy life insurance has been around for decades. I call it L&L because you are liquidating a portion of the IRA and leveraging that money to buy life insurance (usually a 2nd-to-die).

L&L Example

The best way to understand the math of this concept is with an example.

-Couple, both age 62 (H in good health; W in excellent health); one child age 32

-Life expectancy is 87 for H and 91 for the W

–$350,000 in a non-qualified brokerage account AND $1.5 million in a tax-deferred IRA

-$70,000 in combined Social Security Income

-$125,000 in expenses this year; NO state income tax

-2.7% inflation, COLA, saving rate, and income tax bracket inflation

-6% net rate of return on investments

2nd-to-die life—a $12,882 annual premium will buy the parents $1 million in tax-free death benefits through age 100.

Scenario #1—do NOTHING (no conversion, no L&L)

Scenario #2—the “best” Roth IRA conversion numbers

Scenario #3—do NOT convert and use L&L

The following are the numbers assuming the wife is the 2nd to die at age 91.

Which one is better? L&L was significantly better than the Roth conversion example and, in terms of total assets, slightly worse than the do-nothing scenario.

FYI, while the Roth conversion was a financial loser when it comes to total assets while alive, the legacy “net” positive benefit to the heir ended up being $344,903 at the END of the 10-year inherited time frame (meaning the heirs would be better off if the parents converted).

Is the do-nothing example the best outcome? No!

Why? Because in the L&L example, there is $1 million tax-free to the heir, and in the do-nothing scenario, there is $963,000 more in assets in a tax-deferred RIA (FYI, there is also $79,000 more in the non-qualified brokerage account).

Would the heir rather have $142,000 more in total assets when 92% of it is in tax-deferred assets, or $142,000 less when 40% of the money is tax-free?

I’ve run the numbers, and no matter if the heir cashes all the money in the day received, slowly takes withdrawals over time, or waits 10 years to take the money out of the tax-deferred IRAs, the L&L scenario wins!

What can be learned from this newsletter?

1) As I’ve been stating for years, Roth conversions don’t work for most clients (although the heir would be better off vs. the do-nothing scenario).

2) L&L can work to pass more wealth to the heirs vs. Roth conversions AND the do-nothing scenario (this is age and health dependent on the parent(s)).

3) You can run these numbers in 5 minutes in our OnPointe Retirement Planning software.

Roccy’s 1st Annual AI Investment Research and Portfolio Design Survey

13 Questions (3 Minutes)

I had nearly 200 advisors take the survey last week. If you would like to take the survey (those who fill it out will get the results), click on the following link to start the survey:

https://s.surveyplanet.com/7cmogzaw